Equity Financial Group | Investments | Estate Planning | Insurance

Blog

What’s Required of the Executor of an Estate?

April 15, 2024

Being named as the executor of a friend’s or family member’s estate is generally an honor, but settling an estate can be a difficult and time-consuming job. Each state has specific laws detailing an executor’s responsibilities.

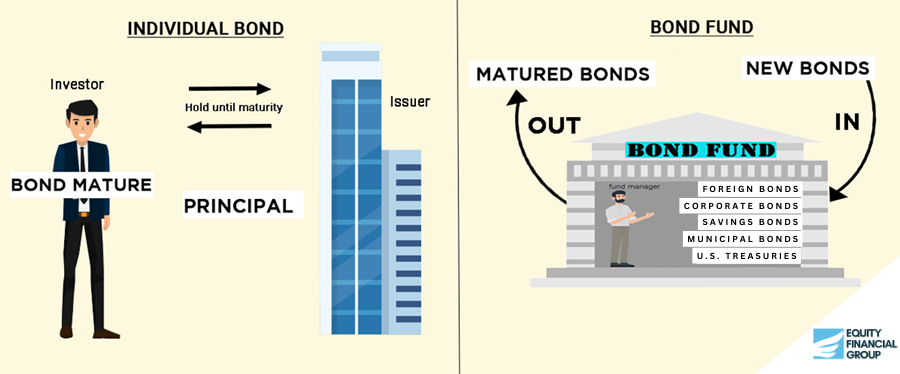

Understanding the Distinctions Between Individual Bonds and Bond Funds

April 8, 2024

Investing in bonds is a popular strategy for generating income, particularly among those seeking a blend of stability and returns in their investment portfolio. However, within the bond market, investors face a choice between individual bonds and bond funds, each offering distinct features, risks, and benefits. This detailed exploration aims to shed light on these differences, enhancing your understanding and aiding in making an informed decision suited to your financial goals. The Core Differen

Exploring the Key Retirement and Tax Adjustments for 2024

March 26, 2024

Exploring the Key Retirement and Tax Adjustments for 2024As the calendar turns, the Internal Revenue Service (IRS) rolls out its annual adjustments in response to inflation, impacting how Americans manage their finances, from retirement savings to taxation. The 2024 adjustments touch on several key areas, including estate and gift taxation, standard deductions, Individual Retirement Accounts (IRAs), employer-sponsored retirement plans, and the kiddie tax...

Rethinking Retirement Savings: The Impact of SECURE 2.0 Act on Roth 401(k) Plans

March 11, 2024

As the landscape of retirement saving undergoes a significant transformation, the SECURE 2.0 Act, part of the sweeping federal spending bill passed in late 2022, stands at the forefront of this change. This legislation introduces critical adjustments to workplace retirement accounts, promising to shape the way Americans think about and prepare for their retirement years. Particularly, it casts a spotlight on Roth 401(k) accounts, offering intriguing opportunities for those in their peak earning

The Federal Reserve’s rapid series of interest rate hikes throughout 2022 and 2023 — initiated in an effort to bring down red-hot inflation — rippled throughout financial markets and the broader economy. People pay attention to the “Fed” to see where interest rates are headed, but also for its economic analysis and forecasting. Members of the Federal Reserve regularly conduct economic research, give speeches, and testify about inflation and unemployment, which can provide clues about where the e

Have you opened an IRA? Getting started early on your retirement savings can have a huge impact. Learn more on the advantages of starting early on your retirement, and how you can begin the journey yourself.

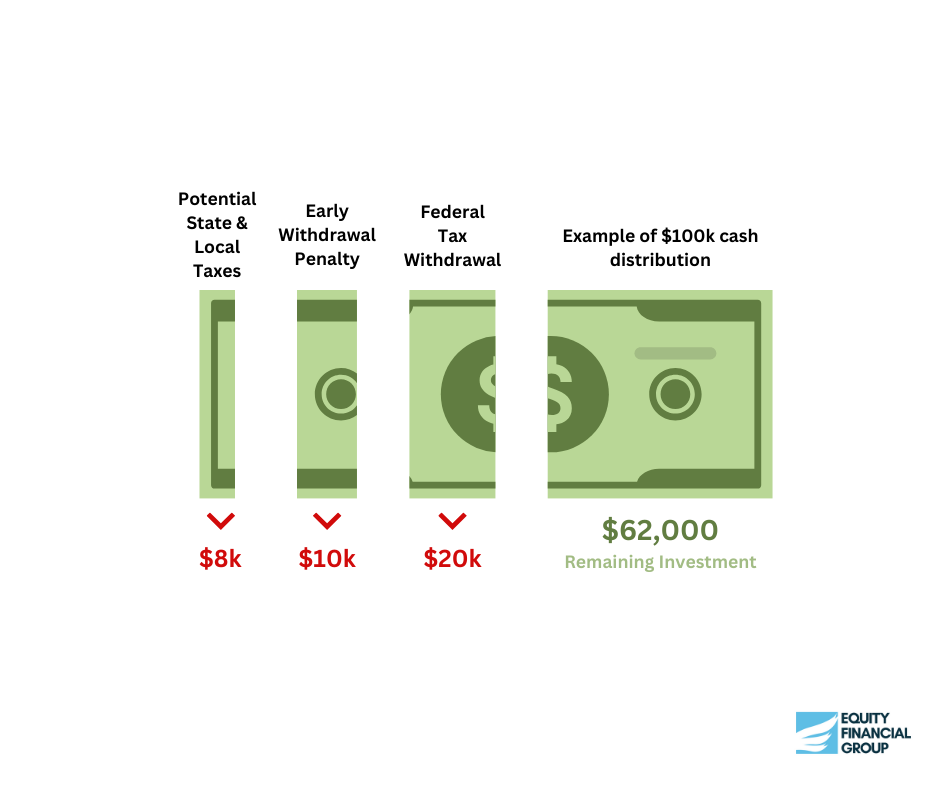

Making an early withdrawal from your 401(k) retirement plan can have significant financial consequences, both immediately and in the long term. This decision can impact your savings and investment growth, affecting your financial security during retirement. Understanding the costs and strategic ways to mitigate them is crucial for anyone considering tapping into their 401(k) prematurely. Immediate Financial Impacts The 10% Early Withdrawal Penalty Withdrawing from your 401(k) before reaching t

Enhancing Retirement Security: Addressing 401(k) Plan Leakage

February 12, 2024

The phenomenon of 401(k) plan "leakage" - where workers withdraw savings from their retirement accounts upon changing jobs - poses a significant challenge to financial security in retirement. Annually, billions are withdrawn prematurely from these tax-advantaged accounts, undermining the potential growth of retirement savings. This article delves into the root causes of leakage, its impact, and the

Setting a Robust Retirement Savings Goal: A Comprehensive GuideUnderstanding your retirement target is crucial, yet surprisingly, only about half of the workers or their spouses have attempted to calculate the savings required for a comfortable retirement. This comprehensive guide aims to bridge this gap by providing a detailed approach to setting a retirement savings goal.Establishing Your Retirement Income NeedsYour post-retirement income needs are unique, yet a general rule of t

Exploring the Impacts of SECURE 2.0 on Retirement Savings in 2024

January 22, 2024

The SECURE 2.0 Act, a comprehensive reform of U.S. retirement savings laws enacted in December 2022, has ushered in a series of significant changes that began to take effect in 2023 and continue into 2024. This landmark legislation has introduced novel features aimed at enhancing the retirement security of Americans. Below is a detailed examination of the key provisions that are influencing retirement planning in 2024.New Opportuni

Life Insurance Essentials: Smart Strategies for Choosing Life Insurance

January 10, 2024

Life insurance stands as a critical component in financial planning, offering a safety net for your loved ones in the event of your untimely passing. Given the potential earnings over a lifetime, securing this asset is essential for the financial security of your family. Understanding the various types of life insurance is key to making an informed decision that aligns with your needs and goals. Understanding the Basics of Life Insuran

When to Stay and When to Go: The Financial Advisor Relationship

January 8, 2024

In the intricate dance of financial planning, your advisor plays a pivotal role. They are your guide through the maze of market trends, investment options, and economic forecasts. But what happens when the music stops aligning with your rhythm? Understanding why clients part ways with their financial advisors and how to gracefully exit this professional relationship is crucial for your financial well-being. Why Clients

The Language of The Stock Market: A Guide to Stock Ticker Symbols

December 26, 2023

Stock ticker symbols—every publicly traded company has at least one—are a key ingredient in the daily market “alphabet soup” scrolling across your screens. Ticker symbols can help investors decipher and simplify complex, fast-moving markets. Stock market ticker symbols compress often lengthy corporate names into a few letters and represent a shared language or shorthand established decades before TV or the internet. When watching financial news services, you’ll often see a company’s ticker symb

RMD Redux: Unpacking the Latest Retirement Distribution Changes

December 18, 2023

The landscape of retirement savings underwent a significant transformation with the passage of the SECURE 2.0 Act in late 2022. This groundbreaking legislation introduced several pivotal changes affecting retirement savings plans, particularly focusing on Required Minimum Distributions (RMDs). This article aims to demystify these changes and offer a straightforward guide on calculating you

In the dynamic world of personal finance, Multi-Year Guaranteed Annuities (MYGAs) have emerged as a compelling investment choice, particularly for those seeking stability and efficiency in growing their savings for retirement. MYGAs stand out for offering a unique blend of safety, competitive returns, and tax efficiency, distinguishing them from traditional investment vehicles like bonds and Certificates of Deposit (CDs). This article explores the distinct advantages of MYGAs, highlighting why t

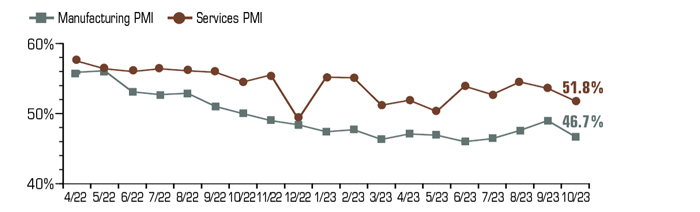

ISM Indexes Reveal U.S. Economy's Dual Dynamics in Manufacturing and Services

December 4, 2023

The Institute for Supply Management (ISM) serves as a crucial barometer for the health of the U.S. economy, providing insights that are invaluable for economists, investors, and businesses alike. Two of its primary tools are the Manufacturing Purchasing Managers Index (PMI) and the Services PMI, each offering a unique window into different sectors of the economy.Manufacturing PMI: A Sign of Economic Health The Manufacturing PMI is a vital indicator, particularly for gauging the condition of U.S.

Receiving an inheritance is a significant event that can impact your financial future. However, it's crucial to approach this situation with thoughtful planning and informed decisions. This article offers a detailed guide to help you navigate the complexities of managing an inheritance effectively. Understanding the Impact of InheritanceInheriting assets can be both a blessing and a responsibility. It's essential to recognize the importance of making well-informed decisions to maxim

When you purchase a fixed-indexed annuity, you have the opportunity to select from indexed strategies that offer you the opportunity to earn interest based, in part, on market performance without the risk of market loss. Funds in an indexed strategy earn interest based, in part, on the positive performance of an external index, such as the S&P 500®. Interest is credited on the last day of each of the strategy’s term and is guaranteed to never be less than 0%. The credited interest is locked int

Maximize Your Savings Potential with Exciting Opportunities!

November 24, 2023

In the world of savings and investment, grabbing opportunities that offer a substantial return is key. That's why we're excited to bring to your attention two different ways to grow your money - including a 13%* Premium Bonus, and also impressive MYGA rates of up to 6.00%* GTD Yield. The MYGA rates offer a fixed interest rate for the term of the contract, ensuring that your investment is not subject to the volatility of the market. This is an excellent chance for those who prefer stability and

Yielding Insights: Understanding Risks in an Evolving Bond Market

November 20, 2023

Yielding Insights: Understanding Risks in an Evolving Bond Market The landscape of bond investing has become increasingly attractive as yields have risen, presenting an opportunity for investors with varying risk tolerances. Bonds offer a blend of stability and income, making them particularly appealing to retirees and those close to retirement who are looking to realign their portfolios. Although traditionally seen as lower risk compared to stocks, bonds are not free from danger. Investors mus

Understanding Tax-Loss Harvesting Tax-loss harvesting is an investment strategy that can turn investment losses into tax deductions, potentially reducing an investor's tax liability. This approach is beneficial when dealing with securities that have decreased in value. By selling these underperforming assets, an investor can realize a capital loss, which can then be used to offset capital gains from better-performing investments or even to reduce taxable income. The Long-Term Benefits of H

Redhawk Wealth Advisors Market Commentary | November 6th, 2023

November 7, 2023

The previous week saw significant gains in the U.S. stock market, with indices posting their largest weekly gains of the year and a strong rebound from recent declines. The NASDAQ increased by 6.6%, the S&P 500 by 5.9%, and the Dow by 5.1%. U.S. Treasury yields fell, with the 10-year Treasury bond yield dropping from 4.83% to 4.52%. Jobs growth showed signs of cooling, which might influence the Federal Reserve to be less aggressive with interest rate hikes. The U.S. economy added 150,000 new...

Exploring the Sustainability of Consumer-Led Economic Growth

November 7, 2023

The robust nature of consumer spending in the United States is a critical engine of economic activity, accounting for approximately two-thirds of the country's gross domestic product (GDP). The resilience of this spending has been a linchpin holding the economy steady amidst the headwinds of persistent inflation and the Federal Reserve's interest rate hikes over the past 18 months. As we approach the holiday season and peer into the horizon of 2024, the question of whether consumer spending can

Redhawk Wealth Advisor's Market Commentary with Rick Keast

November 2, 2023

Are you ready for a deep dive into this quarter’s unique financial landscape? High interest rates are shaking up cash flows, causing many to rethink strategies. While an impressive 72% of companies have beaten EPS estimates through adept cost management, revenues are painting a different picture, declining as businesses grapple with passing inflation onto consumers. This rare divergence between EPS growth and revenue decline hasn’t been seen since at least 2012, signaling that we might be in...

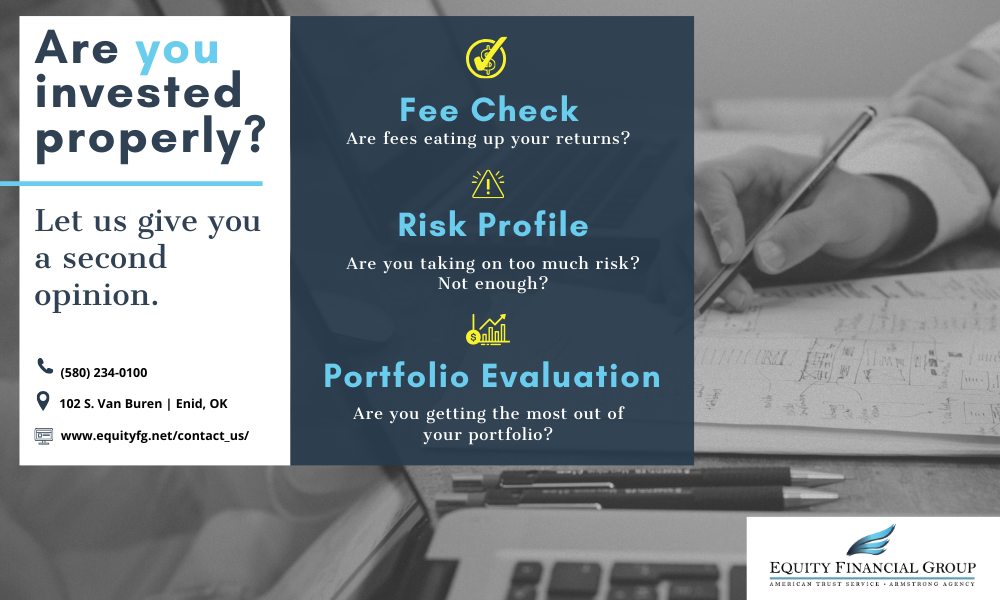

Are You Invested Properly? Let Us Give You A Second Opinion

October 30, 2023

The world of investing can be a labyrinth of choices and strategies, each turn representing a decision that could impact your financial future. It's not uncommon to wonder if your portfolio is on the right track, or if the fees you're paying are worth the services you receive. This is where the value of a second opinion becomes indisputable. a second opinion isn't about doubting your decisions; it's about affirming that you're on the best path for your financial journey or discovering new pa...

Demystifying Variable Annuities: A Comprehensive Guide to Risks and Hidden Fees

October 26, 2023

Variable annuities have garnered popularity as a potential solution for individuals aiming to secure a consistent income stream throughout their retirement years. While they offer unique advantages, their inherent complexity and myriad of associated fees pose significant risks that should not be overlooked. In this comprehensive guide, we aim to unpack the intricacies of variable annuities, shed light on potential dangers, and expose instances where hidden fees have taken a toll on unwary invest

Empowering the Next Generation with a Roth IRATeenagers are no longer just saving up for their next big purchase or weekend outing. With the power of a Roth IRA, these young earners can pave the way for a financially secure future. Whether they're bagging groceries, lifeguarding at the community pool, or taking on seasonal roles, teens can leverage these earnings into a powerful financial tool.Why a Roth IRA for Teens?It’s not just a typical savings account. With a Roth IRA, teens can

Rising Oil Prices Could Pose the Latest Threat to the Economy

October 16, 2023

Rising Oil Prices Could Pose the Latest Threat to the Economy Oil prices have increased more than 30% since late June, driving up transportation costs for consumers and businesses and putting financial markets on edge. On September 27, West Texas Intermediate crude the U.S. benchmark for oil prices topped $93 per barrel, the highest level since August 2022. Brent crude (the global oil benchmark) rose above $96.1 As usual, gasoline prices have followed suit. On September

The Transforming Landscape of Higher Ed: Balancing Cost, Choices, and Challenges

August 28, 2023

Balancing Costs, Choices, and Challenges In the ever-evolving realm of higher education, a recent 2023 survey illuminates a significant shift in public sentiment over the past decade concerning the perceived value of a college degree. A decade ago, 42% of Americans believed that the benefits of a college education outweighed its costs. However, the landscape has changed dramatically, with 56% now expressing doubts due to substantial stu

Mutual Funds: What’s in Your Portfolio? Mutual funds pool investment dollars from many individual investors to purchase a group of selected securities aimed at meeting a particular objective. This offers a convenient way to invest across a wide range of market activity that would be difficult for most investors to do by purchasing individual securities. More than 52% of U.S. households owned mutual funds in 2022.1 Here are some basic types of funds in order of typical risk, from lowest

Is This Bull Market A Sleeping Giant Or A Fierce Matador?

July 31, 2023

June 8, 2023, marked a defining moment in the global financial markets. The S&P 500 index, often seen as a barometer for the US economy, closed at an impressive 4,293.93. This represented a surge of over 20% from its recent bottom at 3,577.03, set on October 12, 2022.1 Such a significant rise is indicative of the transition from a bear market, which began in January 2022, to a bullish phase that kicked off on October 13, 2022.1

Unraveling Jack's Estate: How Probate Struck a Devastating Blow

June 12, 2023

Meet Jack, a diligent individual who had worked hard to build a substantial estate over the years. Unfortunately, Jack passed away unexpectedly without having established a revocable living trust. As a result, his estate had to go through the probate process, leading to significant time and financial losses for his family. 1.) Lengthy and Costly Probate Process: Without a revocable living trust in place, Jack's estate had to undergo probate, which involved a series of court proceedings and

Municipal Bonds: A Tax-Advantaged Way to Put Capital to Work

May 22, 2023

Municipal bonds are issued by public entities such as state and local governments, health systems, universities, and school districts to help finance the building and maintenance of infrastructure projects such as roads, airports, water systems, and facilities. Despite the higher borrowing costs that resulted from the Federal Reserve's inflation-fighting interest-rate hikes, municipalities issued $308 billion in debt in 2022 to fund capital projects, after selling more than $321 billion in

The U.S. stock market struggled in 2022, with the S&P 500 index ending the year down 19.4%. The S&P 500, which includes stocks of large U.S. companies, is generally considered representative of the U.S. stock market as a whole, and it is a good benchmark for broad market performance. But there are thousands of smaller companies, and many of those held onto their stock value better during the market conditions of 2022.

In the past, trusts were often used to avoid estate taxes, but that purpose has become less important for most people with current high exemption amounts ($12.92 million in 2023, $25.84 million for a married couple). However, some states have estate taxes or inheritance taxes with lower exclusion amounts, and a properly constructed trust can serve many other purposes for families of more modest means. A trust might help avoid the time-consuming and costly probate process, maintain control of

Are You Eligible for Any of These College-Related Federal Tax Benefits?

April 17, 2023

Are You Eligible for Any of These College-Related Federal Tax Benefits? College students and parents deserve all the help they can get when paying for college or repaying student loans. If you're in this situation, here are three federal tax benefits that might help put a few more dollars back in your pocket. American Opportunity Credit The American Opportunity tax credit is worth up to $2,500 per student per year for qualified tuition and fees (not room and board) for the first four year

Bank Failures Shine Light on Interest Rate Risks Financial markets reacted turbulently to the collapse of Silicon Valley Bank (SVB) on March 10, 2023, followed two days later by the failure of Signature Bank of New York. With $209 billion in assets and $175 billion in deposits, SVB was the nation's16th largest bank and the second largest to fail in U.S. history. This news was alarming to savers who worried their own bank accounts could be at risk and investors who feared a wider..

If you and your spouse are looking for a way to build your retirement savings but one of you is not working, you might consider funding a spousal IRA. This could be the same IRA that the spouse contributed to while working or it could be a new account. In either case, IRS rules allow a married couple to fund separate IRA accounts for each spouse based on the couples joint income. The total of both IRA contributions cannot exceed the total taxable income rep...

Red Ink: The Debt Ceiling and Deficit Spending On January 19, 2023, the outstanding debt of the U.S. government reached its statutory limit, commonly called the debt ceiling. The current limit was set by Congress at about $31.4 trillion in December 2021. On the day the limit was reached, Treasury Secretary Janet Yellen instituted established "extraordinary measures" to allow necessary borrowing for a limited period of time. While Yellen projects the extension will last until ear

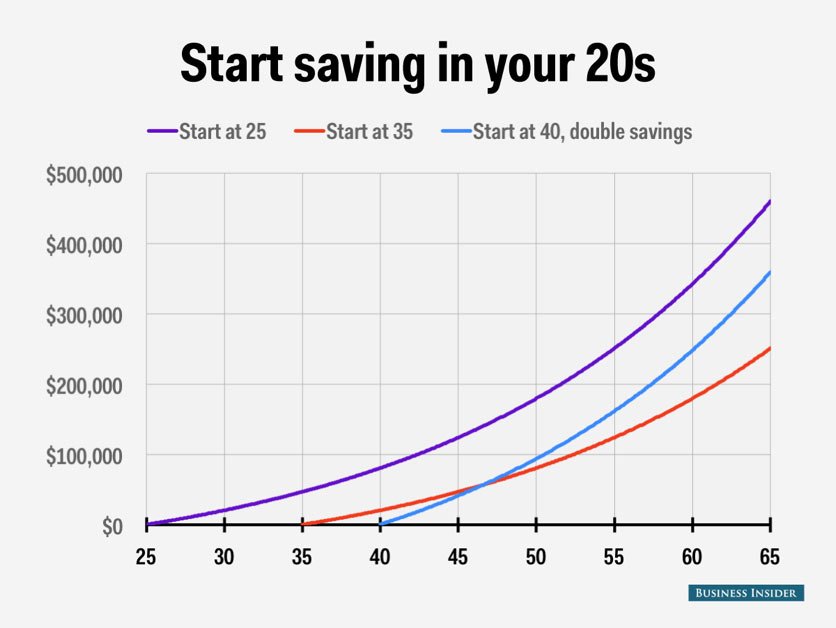

When Should Young Adults Start Investing for Retirement?

March 2, 2023

When Should Young Adults Start Investing for Retirement? As young adults embark on their first real job, get married, or start a family, retirement might be the last thing on their minds. Even so, they might want to make it a financial priority. In preparing for retirement, the best time to start investing is now - for two key reasons: compounding and tax management. Power of Compound Returns A quick Internet search reveals that Albert Einstein once called compounding "the most

With stock and bond markets both faltering over the past year, it’s easy to see why more near retirees have a newfound appreciation for fixed annuities — insurance contracts that guarantee a specified rate of return. A fixed annuity maintains its value regardless of market conditions, and yields on these products have risen in response to the higher interest-rate environment.

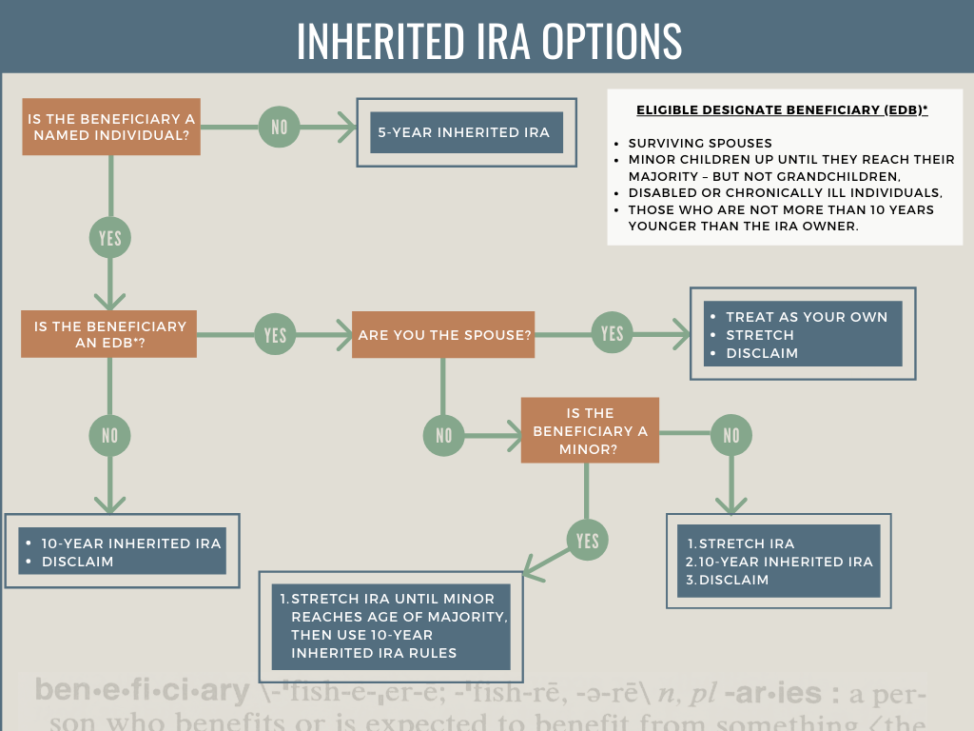

Three Stretch IRA Alternatives The passage of the SECURE Act in 2019 effectively eliminated the stretch IRA, an estate planning strategy that allowed an inherited IRA to continue growing tax deferred, potentially for decades. Most nonspouse beneficiaries, including children and grandchildren, can no longer stretch distributions over their lifetimes. Moreover, proposed IRS regulations require most designated beneficiaries to take annual required minimum distributions (RMDs) within the 10-year di

When you leave your job or retire, you have an opportunity to manage your funds in an employer-sponsored retirement plan such as a 401(k), 403(b), or government 457(b) plan. Depending on the situation, you generally have four options. Rollover The approach that gives you the most control over the funds is to transfer some or all of the assets to an IRA through a rollover. IRAs typically offer a wider variety of investments than employer plans and enable you to consolidate your retirement asse

What Will Happen To Your Estate, When You're Gone?

January 9, 2023

Lets talk about the big elephant in the room... death. Nobody likes to talk about dying, let alone their loved ones dying, but in all reality it is one of the more imporant topics you can discuss. Why you might ask? Whenever somebody dies, they leave behind

A will is a legal document that outlines how you want your assets to be distributed and managed after your death. It also allows you to name an executor who will be responsible for carrying out your wishes and guardians for any minor children. While you can use a will to leave assets to your heirs, it may not be the most efficient method for doing so. A trust, on the other hand, is a legal arrangement in which a person or organization (the trustee) holds a

Long-term bonds generally provide higher yields than short-term bonds, because investors demand higher returns to compensate for the risk of lending money over a longer period. Occasionally, however, this relationship flips, and investors are willing to accept lower yields in return for the relative safety of longer-term bonds. This is called a yield curve inversion, because a graph showing bond yields in relation to maturity is essentially turned upside down...

Fraudsters and Scammers Pocket Nearly $6 Billion in 2021

December 19, 2022

Fraudsters and Scammers Pocket Nearly $6 Billion in 2021 According to the Federal Trade Commission (FTC), 2.8 million people lost $5.8 billion to fraud in 2021, a 70% increase in losses over 2020. Imposter scams topped the list of fraud types, surpassing others by a huge financial margin, followed by online shopping scams. Nearly 1 million consumers lost more than $2.3 billion to imposter scams, with a median loss of $1,000. Imposter scams happen when an individual posing as someone else...

IRA Distributions Can Benefit Your Favorite Cause … and Your Tax Bill

December 12, 2022

As the number of itemizers fell, so did the amount individuals gave to charities as a percentage of total annual contributions. According to Giving USA, the total amount dropped below 70% for the first time ever in 2018 and remained there through 2021.

The U.S. stock market had a banner year in 2021, with the S&P 500 index up almost 27%. Unfortunately, stocks turned downward on the second trading day of 2022 and kept sliding into a bear market. Stocks in the S&P 500 are classified by 11 different business sectors, each of which responds differently to economic conditions. For example, the information technology sector was very strong in 2021, rising by 33.4%. But it turned south in 2022 and dropped by 26.7% through October.

’Tis the Season for Tax-Friendly Giving Strategies

December 1, 2022

You may donate money to charitable organizations throughout the year, for no other reason than your heart-felt desire to support causes that you care about. But if philanthropy is important to you, keep in mind that the associated tax breaks could potentially increase your ability to give. You might consider a more strategic approach to charitable giving, possibly as part of your year-end tax planning. You can generally deduct charitable contributions, which reduces your taxable income, only if

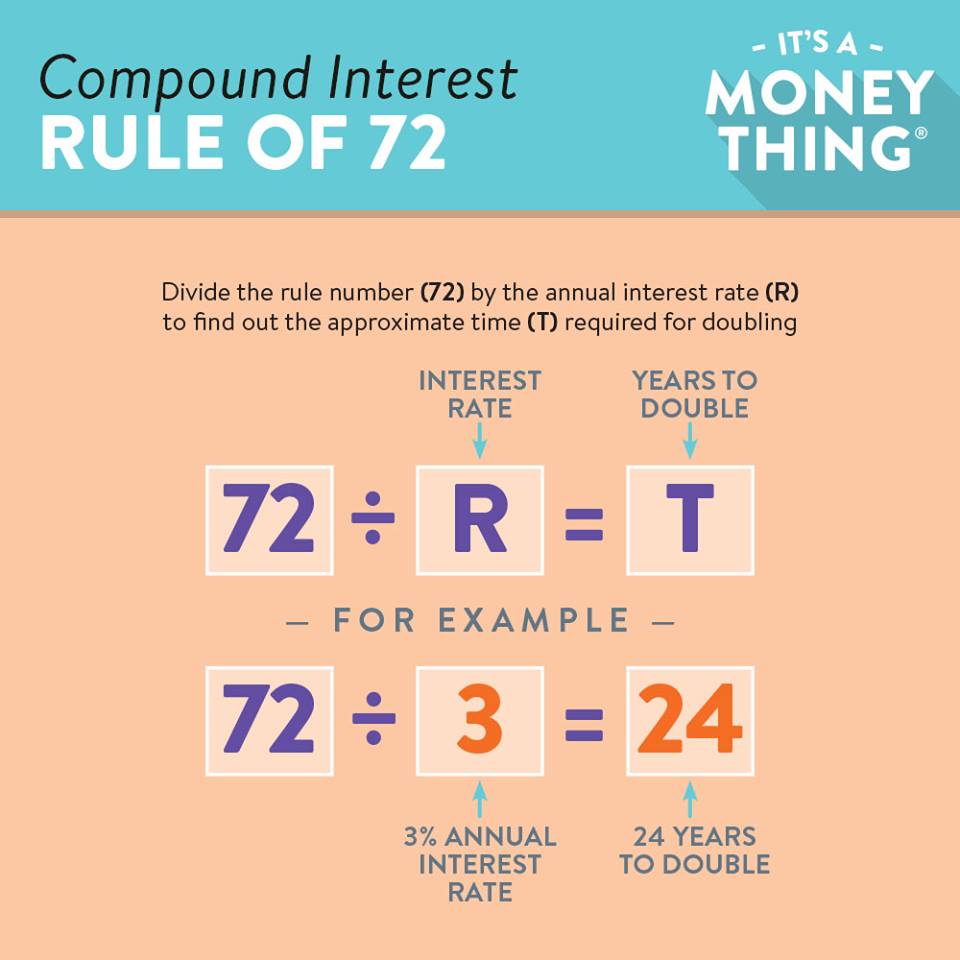

Before making any investment decision, one of the key elements you face is working out the real rate of return on your investment.Compound interest is critical to investment growth. Whether your financial portfolio consists solely of a deposit account at your local bank or a series of highly leveraged investments, your rate of return is dramatically improved by the compounding factor.With simple interest, interest is paid just on the principal. With compound interest, the return that you receive

Life insurance can serve many valuable purposes. However, later in life — when your children have grown, you’ve retired, or you’ve paid off your mortgage — you may no longer think you need to keep your coverage, or perhaps your coverage has become too expensive. You might be tempted to abandon the policy or surrender your life insurance coverage, but there are other alternatives to consider.

If you worry about your retirement investments during market downturns, you're not alone. Unfortunately, emotions are often the enemy of sound investing. Here are some points to help you stay clear-headed during periods of market volatility. Markets Rebound Historically, even the worst bear market has bounced back and eventually gone on to reach new highs. In fact, since 1970, bear markets have lasted an average of 14 months. A Chance to Buy Low If you're investing a set amount of...

The importance of proper estate planning cannot be overstated, regardless of the size of your estate or the stage of life you're in. Nevertheless, it's surprising how many American adults haven't put a plan in place. You might think that those who are rich and famous would be way ahead of the curve when it comes to planning their estates properly. Yet plenty of celebrities and people of note have died with inadequate or n

What Does a Strong Dollar Mean for the U.S. Economy?

November 9, 2022

In late September 2022, the U.S. dollar hit a 20-year high in an index that measures its value against six major currencies: the euro, the Japanese yen, the British pound, the Canadian dollar, the Swedish krona, and the Swiss franc. At the same time, a broader inflation-adjusted index that captures a basket of 26 foreign currencies reached its highest level since 1985. Both indexes eased slightly but remained near their highs in October. Intuitively, it might seem that a strong dollar

CHIPS and Science Act Aims to Preserve U.S. Technology Edge

October 31, 2022

The CHIPS and Science Act of 2022, signed into law on August 9, is bipartisan legislation that provides more than $50 billion in direct financial assistance for companies to increase U.S.-based semiconductor design, research, and manufacturing capabilities. In addition, the legislation authorizes nearly $170 billion in federal funding over five years for research and development R&D programs in strategic areas of science and technology, such as artificial intelligence, quantum computing...

Throughout your life, your financial needs will change, and life insurance can help you meet some of those needs. But how much life insurance do you need? There are a number of approaches to help determine how much life insurance you should have. Here are three of those methods:

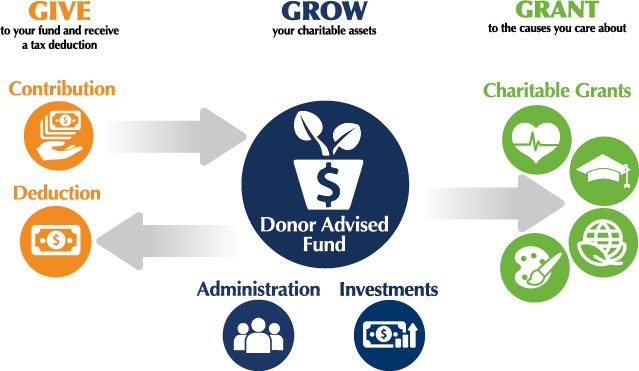

Donor-Advised Funds Combine Charitable Impact with Tax Benefits

October 24, 2022

Donor-Advised Funds Combine Charitable Impact with Tax Benefits A donor-advised fund (DAF) is a charitable account offered by sponsors such as financial institutions, community foundations, universities, and fraternal or religious organizations. Donors who itemize deductions on their federal income tax returns can write off DAF contributions in the year they are made, then gift funds later to the charities they want to support. DAF contributions are irrevocable, which means the donor gives the

Index funds, which try to match the performance of a particular market index, have drawn increasing interest from investors, but traditional actively managed funds still hold more assets (see chart). There is ongoing discussion in the financial media about which approach is most effective, but there may be good reasons to hold both in a well-diversified portfolio. Here are some pros and cons to consider:

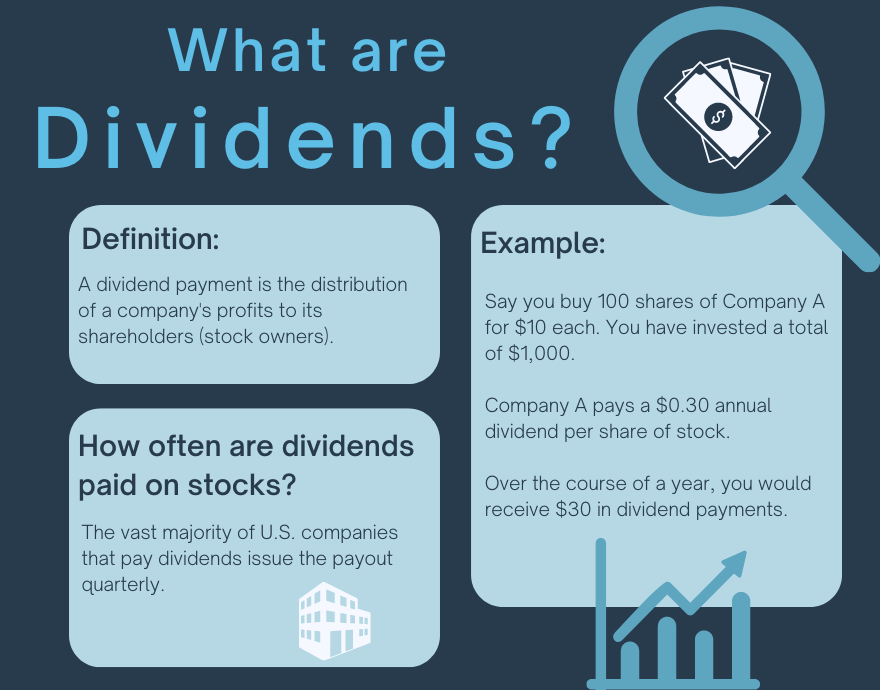

John D. Rockefeller, one of the wealthiest Americans in history, loved receiving stock dividends. "Do you know the only thing that gives me pleasure?" he once asked. "It's to see my dividends coming in." There may be many things other than money that give you pleasure, but you can still appreciate the stabilizing role that dividends might play in your portfolio. Steady and Dependable Dividends can be a dependable source of income

Unpacking the Inflation Reduction Act: What’s in It?

September 6, 2022

Unpacking the Inflation Reduction Act: What's in It? The Inflation Reduction Act (IRA), signed into law on August 16, 2022, is a package of climate, energy, health-care, and tax legislation. It authorizes about $440 billion in new spending and will generate an estimated $740 billion in revenue and savings, reducing the deficit by around $300 billion over a decade.1 About $370 billion will fund new and existing programs that aim to expand renewable energy sources and help mitigate the ne

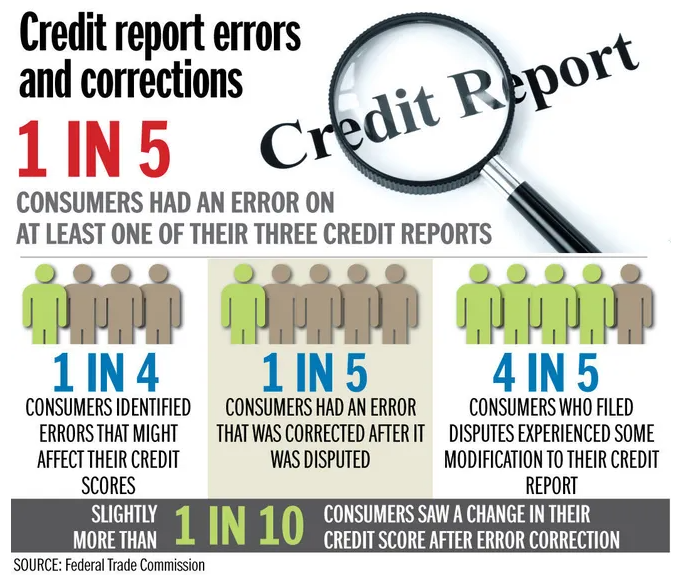

How to Correct an Error on Your Credit Report According to the Consumer Financial Protection Bureau (CFPB), credit report errors more than doubled during the coronavirus pandemic. In addition, the CFPB found that many pandemic protections which were designed to help consumers, such as loan forbearance periods on federal student loans and federally backed mortgages, ended up negatively impacting their credit reports as a result of complications such as processing delays and suspended payments be

Sticker Shock Is No Joke for Car Buyers The average price for a new vehicle reached $47,077 in December 2021, which amounts to a 14% price hike in just one year. Perhaps more startling, the average price paid for a nonluxury vehicle was $900 above the Manufacturer Suggested Retail Price (MSRP), otherwise known as the sticker price.1 Most people who have shopped for a new car in recent months can attest to the meager selection of available cars offered at sky-high prices.

Inflation Protection for Investment Dollars For the 12-month period ending in June 2022, the Consumer Price Index for All Urban Consumers (CPI-U) the most widely used measure of inflation increased 9.1%, the fastest pace in more than 40 years. The rate may trend downward as the Federal Reserve raises interest rates and supply-chain issues improve. But inflation is likely to be relatively high for some time. High inflation not only hits consumers in the pocketbook for cur...

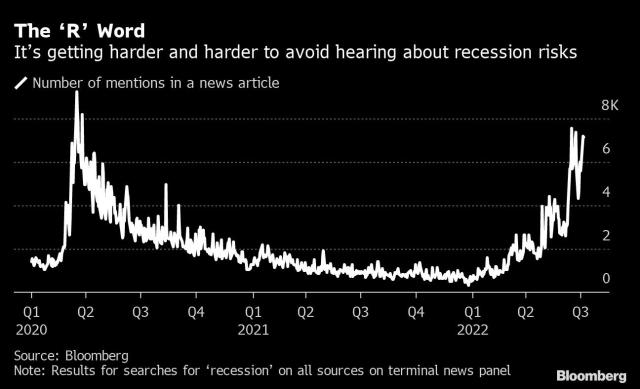

Is the U.S. Economy in a Recession? In an early July poll, 58% of Americans said they thought the U.S. economy was in a recession, up from 53% in June and 48% in May. Yet many economic indicators, notably employment, remain strong. The current situation is unusual, and there is little consensus among economists as to whether a recession has begun or may be coming soon. Considering the high level of public concern, it may be helpful to look at how a recession is officially determined an

A Wealth of Information: How to Read a Mutual Fund Prospectus

July 18, 2022

A Wealth of Information: How to Read a Mutual Fund Prospectus With more than 7,400 mutual funds to consider in the United States alone, some investors may feel overwhelmed by the thought of deciding which ones to select for their portfolios. At the same time, most mutual fund-owning households base their purchase decisions on these measures: historical performance (94%), investment objectives and risk potential (91%), and fees and expenses (90%). Fortunately, reading a mutual fund pros

Tech Sector Turmoil and the Bear Market During the intensely volatile first 100 trading days of 2022, the stocks of companies in the S&P 500 index delivered their worst performance since 1970. The S&P 500 continued to tumble, and the benchmark index descended into a bear market - typically defined as a sustained drop in stock prices of at least 20% - on June 13, 2022. When the market closed, the S&P 500 had dropped 21.8% from its January 3 peak, and the tech-heavy D

Imagine stepping into an elevator and realizing that you’re about to spend the 30-second ride with someone who could make your retirement dreams come true — if only you could explain them before the doors open again. How would you summarize your financial situation, outlook, aspirations, and plans if you had 30?seconds to make an “elevator pitch” about achieving one of your most important goals?

Avoiding Probate Probate is the process of proving the validity of a will and supervising the administration of an estate, usually in the probate court. State law governs the proceedings in the probate court, so the process can vary from state to state. Supervising the administration of an estate can result in additional expense, unwanted publicity, and delays in the distribution of estate assets for a year or longer, which is why planning to avoid the probate process may be beneficial. There..

High Inflation: How Long Will It Last? In March 2022, the Consumer Price Index for All Urban Consumers (CPI-U), the most common measure of inflation, rose at an annual rate of 8.5%, the highest level since December 1981. It's not surprising that a Gallup poll at the end of March found that one out of six Americans considers inflation to be the most important problem facing the United States.2 When inflation began rising in the spring of 2021, many economists, including policymakers

As measured by the Consumer Price Index for food at home, grocery prices increased 3.4% in 2020, a faster rate than the 20-year historical average of 2.4%.1 More recently, food inflation accelerated by 6.5% during the 12 months ending in December 2021, while prices for the category that includes meat, poultry, fish, and eggs spiked 12.5%.2 Food prices have long been prone to volatility, in part because the crops grown to feed people...

Every year, the Internal Revenue Service announces cost-of-living adjustments that affect contribution limits for retirement plans and various tax deduction, exclusion, exemption, and threshold amounts. Here are a few of the key adjustments for 2022. Estate, Gift, and Generation-Skipping Transfer Tax The annual gift tax exclusion (and annual generation-skipping transfer tax exclusion) for 2022 is $16,000, up from $15,000 in 2021.The gift and estate tax

Colliding Forces: Russia, Oil, Inflation, and Market Volatility

March 7, 2022

Colliding Forces: Russia, Oil, Inflation, and Market Volatility The Russian invasion of Ukraine has drawn condemnation and punitive sanctions from the United States, Europe, and their allies. The humanitarian cost of war cannot be measured, and the long-term economic effects could take months or years to unfold. However, the early stages of the conflict pushed oil prices upward and sent the U.S. stock market plunging, only to see stocks bounce back and drop again...

The headline U.S. unemployment rate fell from 6.7% at the end of December 2020 to 3.9% in December 2021 — the biggest one-year improvement in history.1 While many workers took advantage of this strong rebound in the job market, companies large and small have been struggling with labor shortages.

The critical question an investor should be asking themselves is if they want a sales representative investing assets that will impact their standard of living during retirement and their financial security late in life?

Making long-term decisions about money can be difficult and even a little scary. Many people turn to an advisor for help with their financial decisions. Many advisors offer good advice but deciding whether they're worth the price can be difficult. Before an investor hires an advisor, they should make sure that the advisor has their best interests in mind. There are many benefits to hiring an advisor as they often have a broader, deeper knowledge of money...

Investors simply can't have it all (risk free). To get a reward, investors must be willing to accept some risk. That is the fundamental trade-off of investing; risk is involved with almost any investment. Investors must establish their establish their investor personality to structure their investment strategy.

Net Price Calculators Help Gauge College Affordability

November 15, 2021

Net Price Calculators Help Gauge College Affordability Fall is the time when many high school seniors narrow their college lists and start applying to colleges. One question that is often front and center on the minds of families is...

Covering relevant topics for what lies ahead throughout the week of November 8th-12th, while summarizing what happened during last week's earnings frenzy. Rick takes a dive into relevant economic data, including rising inflation, tapering, the Consumer Price Index, and more.

How To Thrive, Not Just Survive, In The Post Covid World

November 8, 2021

The fallout from the COVID-19 pandemic creates the need for a new type of financial advisor who can integrate digital marketing tools, use video conferencing to close business, provide virtual client servicing, and more.

NFTs and Blockchain: What You Should Know About the Digital Collectibles Craze

November 1, 2021

In March 2021, a digital image by a graphic artist known as Beeple was sold in the form of a nonfungible token, or NFT, for $69.3 million, making him the third-most-valuable living artist. This was the first sa...

Annuities are insurance-based financial vehicles that can provide many benefits sought by retirement-minded investors. There are a number of reasons why people buy annuities. Deferral of taxes is a big benefit, and so is the ability to put large sums of money into an annuity — more than is allowed annually in a 401(k) plan or an IRA — all at once or over a period of time. Annuities offer flexible payout options that can help retirees meet their cash-flow needs.

Unfortunately, placing all your savings in taxable instruments like certificates of deposit can create quite an income tax bill. In an effort to help provide stability, some investors inadvertently produce a liability. It’s a bit like turning on all the taps in your house just to make certain the water is still running. Sure, you’ll know that the water is still running, but a lot of it will go down the drain. The solution is simply to turn off some of the taps.

Don't Let Debt Derail Your Retirement Debt poses a growing threat to the financial security of many Americans - and not just college graduates with exorbitant student loans. Recent studies by the Center for Retirement Research at Boston College (CRR) and the Employee Benefit Research Institute (EBRI) reveal an alarming trend: The percentage of older Americans with debt is at its highest level in almost 30 years, and the amount and types of debt are on the rise. Debt Profile of Older

"Financial planning” is an umbrella term that can be applied to various aspects of money management. Many people associate financial planning with retirement. However, effective financial planning can help people confront today’s challenges just as much as it can help them prepare for their golden years.

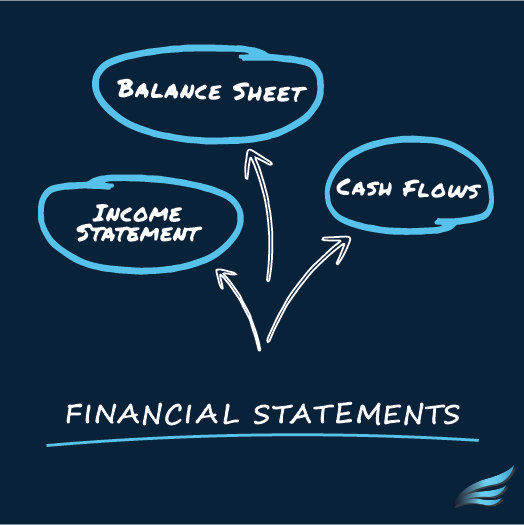

Understanding company fundamentals is a key component when it comes to making smart investment decisions. Learn more about what are widely considered to be "The 3 Key" financial statements, with this easy to understand chart.

If you are self-employed or own a small business and you haven't established a retirement savings plan, what are you waiting for? A retirement plan can help you and your employees save for the future...

During the last week of February 2020, the S&P 500 lost 11.49% — the worst week for stocks since the 2008 financial crisis — only to jump by 4.6% on the first Monday in March...

The Coronavirus Aid, Relief, and Economic Security (CARES) Act was signed into law on March 27, 2020. This $2 trillion emergency relief package represents a bipartisan effort to assist both individuals and businesses in the ongoing Coronavirus Pandemic and accompanying economic crisis. The CARES Act provisions for retirement plan relief for individuals under federal tax law are discussed here.

Paycheck Protection Program (PPP) Loans: What you need to know

April 8, 2020

A Paycheck Protection Program (PPP) loan is part of the $2 trillion CARES Act. The SBA classifies PPP loans as a 7(a) loan with $349 billion* designated for the program. The loans feature a streamlined application process, less documentation and fewer restrictions. If you’re considering such a loan for your business, it’s important to understand who does and doesn’t qualify, how much you can borrow, how forgiveness works and other key details.

CARES Act Provides Relief to Individuals and Businesses

April 2, 2020

On Friday, March 27, 2020, the Coronavirus Aid, Relief, and Economic Security (CARES) Act was signed into law. This $2 trillion emergency relief package is intended to assist individuals and businesses during the ongoing coronavirus pandemic and accompanying economic crisis. Major relief provisions are summarized here. Unemployment provisions The legislation provides for: An additional $600 weekly benefit to those collecting unemployment benefits, through July 31, 2020An additional 13

Rolling over your Employee Retirement Plan Assets can seem like an overwhelming task at times. It's important to understand the basics of these types of plans, as well which type of rollover you will be initiating. In this article find you can find a brief summary of the process you can expect when you begin a rollover.

For most working Americans, the road to retirement is a long haul focused on efficient money management and prudent investing. We spend decades planning, putting money away, and investing in hopes of building a nest egg that will one day grow large enough for us to one day retire. But what happens after retirement?

Why do so many people never obtain the financial independence that they desire? Often it's because they just don't take that first step — getting started.

.png)

.png)

(452 × 381 px) (904 × 762 px).png)

.png)