If you’re a parent or grandparent thinking about your child’s long-term financial future, the new Trump accounts could be one of the most interesting tools to hit the market in years. They’re not a replacement for 529 plans or Roth IRAs, but they offer something unique: the ability to start serious, tax-advantaged investing the day a child is born—without needing earned income.

Here’s the straight talk on how they actually work, where they shine, where they fall short, and—most importantly—how smart families are using them as one piece of a bigger wealth-building strategy.

The “Growth Period”: Compounding Starts on Day One

Trump accounts are scheduled to launch in mid-2026. Once opened, they enter a locked “growth period” that runs from birth through December 31 of the year the child turns 17. During those 18 years:

-

You (and others) can contribute money

-

The account stays fully invested

-

Withdrawals are generally off-limits

That early lock-up is the real power move. Starting at birth gives the money nearly two full decades of uninterrupted compounding before most kids even think about college or their first job. For families who can afford to let the money sit, this is a legitimate edge.Who Can Contribute—and How Much?Here’s what makes these accounts different from almost anything else:

-

Parents, grandparents, and other individuals: Up to $5,000 per year per child

-

Employers: Up to $2,500 per year (counts toward the $5,000 individual limit)

-

Governments or nonprofits: No limit

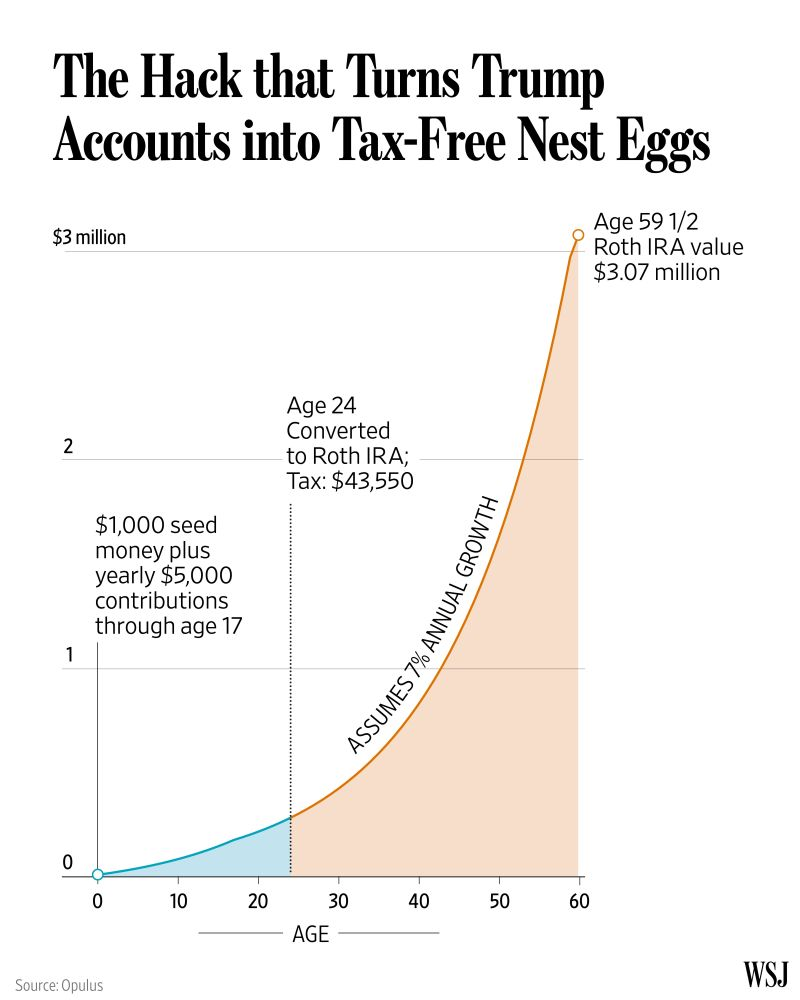

Even better, for kids born between 2025 and 2028, the government is offering a one-time $1,000 “seed” contribution. That’s free money—literally deposited into the account with zero strings attached from the family’s side. Over 18 years of compounding at a conservative 7% return, that single $1,000 could grow to roughly $3,400 before the child even turns 18. Not life-changing on its own, but a meaningful kick-start.

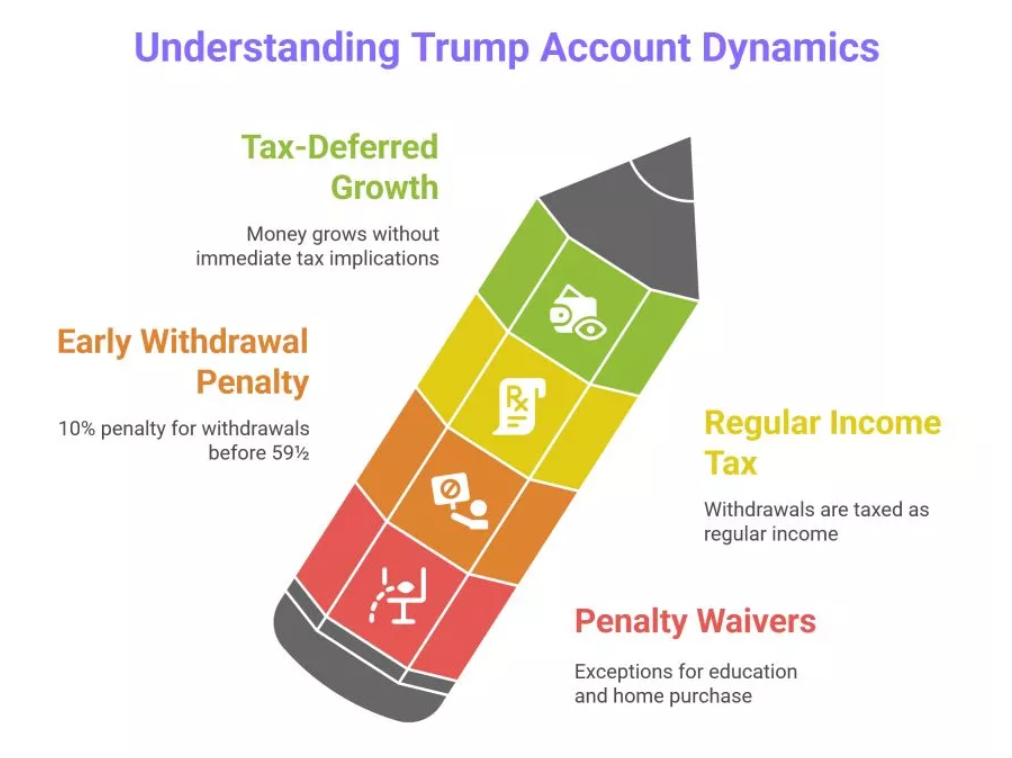

Investment Rules: Simple, Cheap, and (Intentionally) Boring

During the growth period, the account must stay in low-cost, broad U.S. stock index funds or ETFs with expense ratios under 0.10%. No individual stocks, no international funds, no fancy alternatives.This keeps fees tiny and prevents speculative bets with a child’s money—smart design. The trade-off is less diversification than you might choose in your own portfolio. But for long-term growth, a plain-vanilla U.S. total market fund has historically been hard to beat.

How Trump Accounts Compare to What You Already Know

Feature |

Trump Account |

Roth IRA (for a minor) |

529 Plan |

|---|---|---|---|

Needs earned income? |

No |

Yes |

No |

Contributions |

After-tax |

After-tax |

After-tax |

Tax-free growth? |

Only on family contributions |

Yes (full amount) |

Yes (if used for education) |

Early withdrawal rules |

Locked until 18 |

Contributions anytime |

Penalty-free for education |

Best use |

General long-term wealth |

Retirement or flexibility |

College costs |

The big takeaway: Trump accounts are not more tax-efficient than a Roth IRA if your teenager has earned income. But they’re far more flexible than a 529 if the money might not go toward school. And unlike both, they let you start the day the birth certificate is issued.

The Tax Reality Most People Miss

This is the part that separates the good planners from everyone else.Only contributions made by individuals (you, grandparents,  etc.) create “tax basis.” Government seed money, employer matches, and nonprofit gifts do not. That means when the child eventually pulls money out after 18, only the family’s original contributions come out tax-free. Everything else—including all the growth on the government or employer money—is taxed as ordinary income.Quick example most families will recognize:

etc.) create “tax basis.” Government seed money, employer matches, and nonprofit gifts do not. That means when the child eventually pulls money out after 18, only the family’s original contributions come out tax-free. Everything else—including all the growth on the government or employer money—is taxed as ordinary income.Quick example most families will recognize:

-

Family puts in $4,000/year

-

Government adds $1,000 seed

-

Account grows to $40,000 by age 18

Only $4,000 (10% of the total) is tax-free. The rest is taxable on withdrawal. That’s why pairing Trump accounts with other vehicles matters.

After Age 18: Real Flexibility Opens UpOnce the growth period ends, the account becomes much more like a traditional retirement account. The child can:

-

Keep it growing under IRA-like rules

-

Roll it into an existing IRA

-

Convert it to a Roth IRA (especially powerful if they’re in a low tax bracket early in their career)

The Roth conversion strategy is one many wealth advisors are already flagging for clients. A 22-year-old in their first job with modest income could convert at a very low tax rate and then enjoy decades of completely tax-free growth.

Where Trump Accounts Actually Fit in a Real Family Plan

These accounts aren’t a silver bullet—and they don’t need to be. The smartest families treat them as one tool in the toolbox:

-

Use the Trump account for general long-term wealth that isn’t tied to college.

-

Max out 529 plans for education expenses.

-

Fund Roth IRAs for kids with summer jobs or part-time work.

-

Keep some money in plain taxable brokerage accounts for maximum flexibility.

Done right, the Trump account becomes the “set it and forget it” layer that quietly builds serious wealth while you focus on the more immediate goals like college funding or buying that first home.

The Bottom Line for Parents Who Want to Get This Right

~001.png)